A Grey Hybrid Multi-Criteria Decision-Making Framework for Assessing Tax Performance in G7 Economies

DOI:

https://doi.org/10.59543/cssm0s83Keywords:

Tax Performance, G7 Economies, MCDM, Grey SPC, Grey SRPAbstract

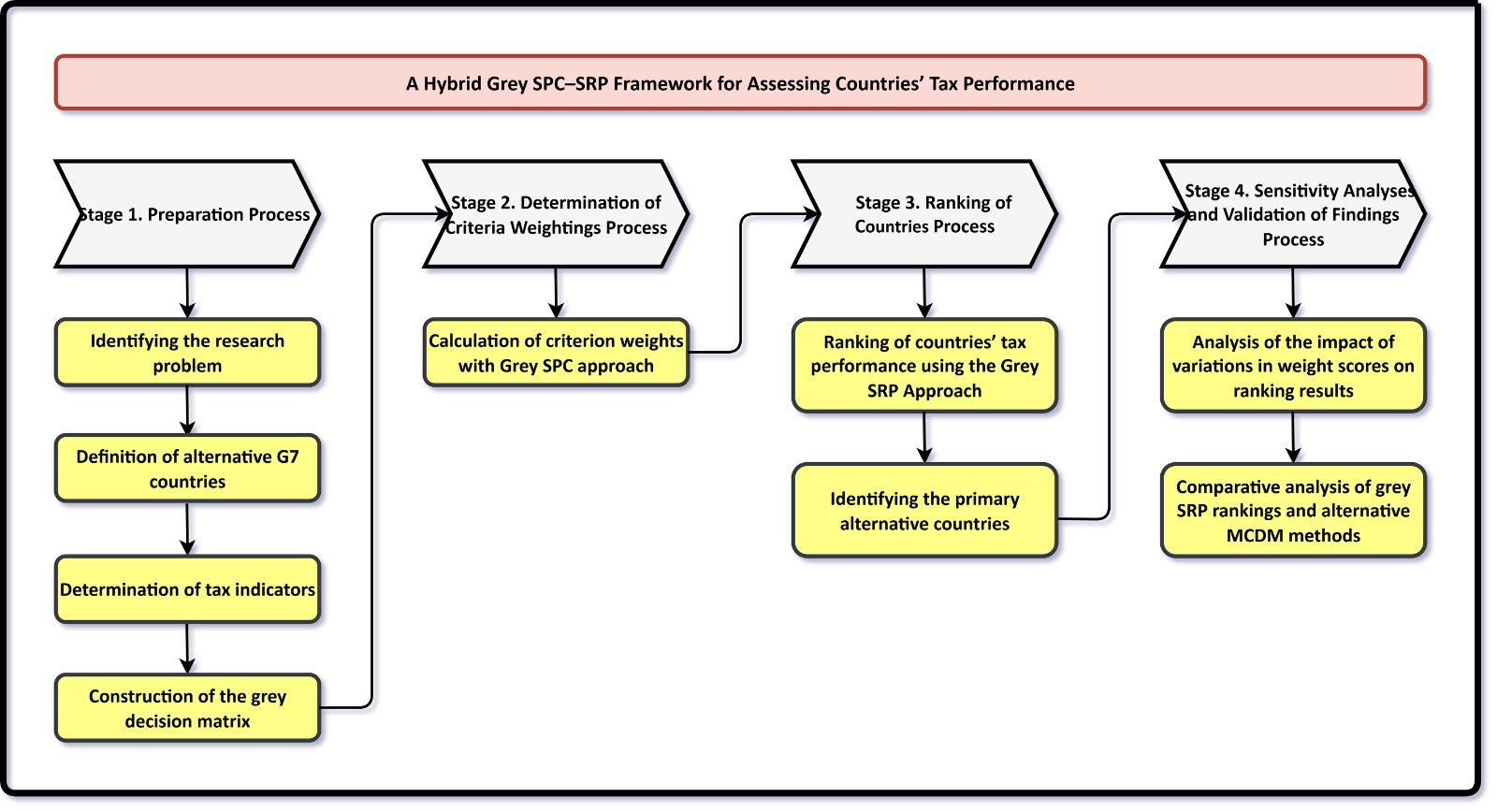

In spite of the fact that tax performance constitutes a central dimension of fiscal governance, its comparative measurement across countries has received limited attention within the multi-criteria decision-making literature. Addressing this gap, the present manuscript proposes an integrated hybrid decision-making methodology — combining the Grey Symmetry Point of Criterion (Grey SPC) and Grey Simple Ranking Process (Grey SRP) methods — for the systematic and comparative assessment of tax performance. The introduced model derives objective criterion weights through the Grey SPC approach and generates country rankings through the Grey SRP technique, ensuring full methodological consistency between the two stages while preserving uncertainty throughout the analytical process via grey interval numbers. The developed approach is empirically applied to the G7 economies using ten-year average data for the period 2013–2022 across four tax performance indicators: total tax revenue, income and profits tax, corporate tax, and goods and services tax. The empirical findings reveal goods and services tax as the most influential criterion, while France attains the highest overall tax performance score among the G7 economies. The robustness of the rankings is confirmed through systematic weight sensitivity analyses and comparisons with five widely adopted grey MCDM methods. Overall, the findings provide useful policy insights for improving fiscal performance through structural reforms in tax composition rather than through a sole emphasis on aggregate revenue levels.

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2026 Berrak Tekgün, Şerife Merve Koşaraoğlu (Author)

This work is licensed under a Creative Commons Attribution 4.0 International License.