The Evolution of Disclosure Narratives in Audit Firms: Evidence from Dynamic Community Detection of Transparency Reports

DOI:

https://doi.org/10.59543/3pw0rs17Keywords:

Transparency reports, Dynamic community detection, Institutional theory, Symbolic complianceAbstract

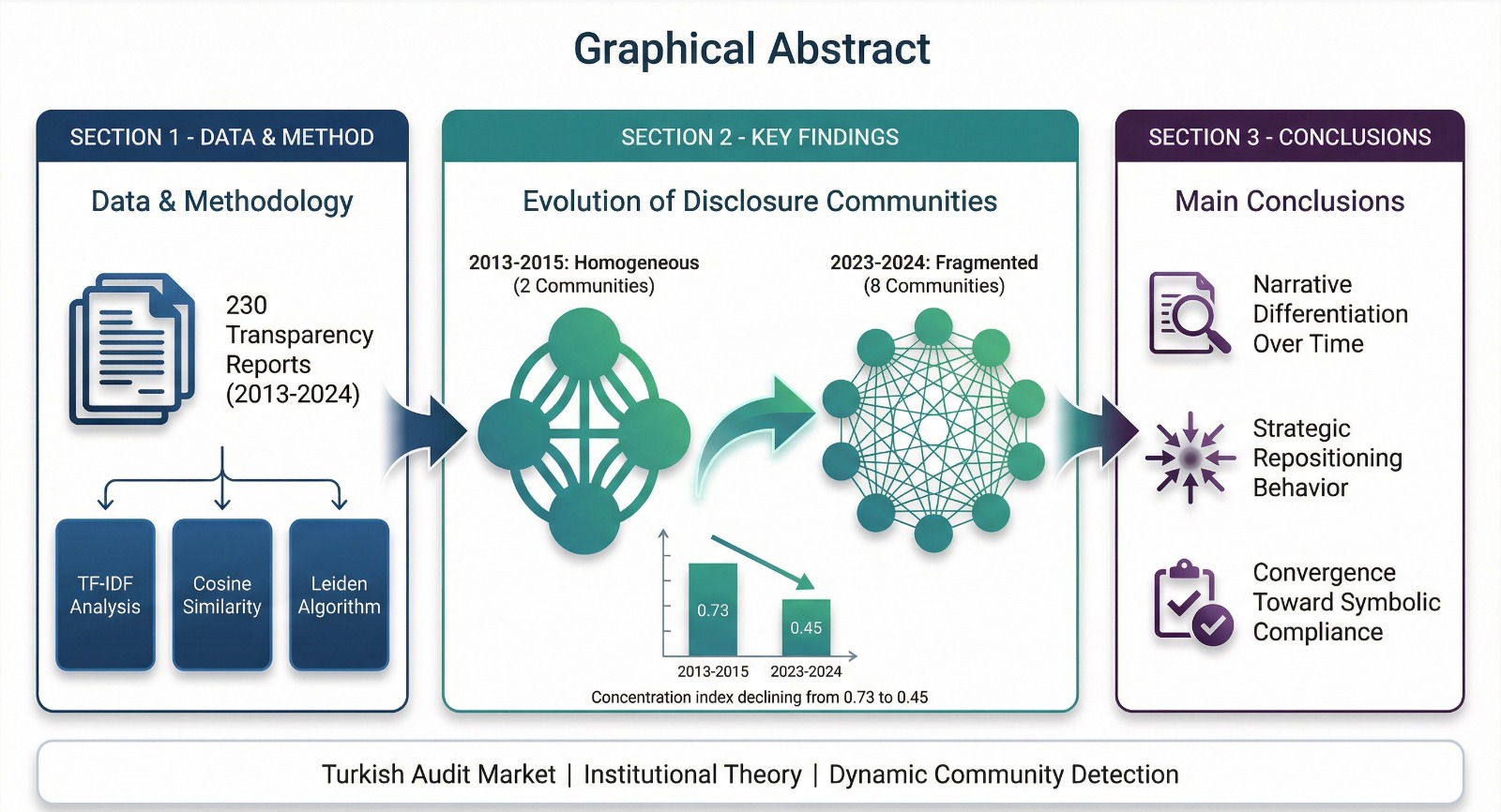

Transparency reporting has emerged as a critical regulatory mechanism for enhancing accountability in the audit profession following prominent corporate scandals. Nevertheless, the literature contests the extent to which these mandatory disclosures provide substantive information rather than serving as symbolic compliance tools. The present study aims to address the existing gap in understanding how audit firm disclosure narratives evolve and how firms strategically reposition themselves within the disclosure landscape. The objective of this research is to examine the longitudinal dynamics of disclosure strategies in Turkish audit firm transparency reports from 2013 to 2024, investigating the emergence of narrative communities and firms' strategic repositioning behaviours. A novel methodological framework is employed, integrating computational text analysis with dynamic network science. Specifically, term frequency-inverse document frequency and cosine similarity measures are utilized to assess narrative proximity between transparency reports. The Leiden algorithm for dynamic community detection is then applied to identify and track disclosure communities across 230 firm-year observations from 89 distinct audit firms. The results reveal a fundamental transformation in the disclosure landscape: an initially homogeneous narrative structure dominated by two generalist communities in early years evolved into a fragmented system comprising eight specialized disclosure communities by 2024. Furthermore, audit firms engage in systematic narrative repositioning, with a pronounced gravitation toward compliance-oriented communities during periods of maximum fragmentation. The results show that mandatory transparency rules can have unintended effects. For example, when narratives become more complex, companies tend to use symbolic, procedure-focused disclosure strategies instead of substantive differentiation. The study offers critical implications for regulators seeking to design disclosure frameworks that foster genuine transparency rather than superficial compliance.

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2026 Abdullah Kürşat Merter, Murat Özcan, Yavuz Selim Balcıoğlu, Mehmet Günlük (Author)

This work is licensed under a Creative Commons Attribution 4.0 International License.